At the Municipality & Public Employer Roundtable on April 24, MedBen Senior Vice President Caroline Fraker discussed mental health parity and how proposed rules are expected to affect self-funded employers in 2025.

“Mental health and substance use disorder benefits must be offered in parity with medical and surgical benefits,” Fraker said. “But while mental health parity has been the law since 1996, how parity is measured has changed.”

Under current law, parity is proven in two ways:

- Quantitative Treatment Limitations (QTLs) – Financial limits on the scope or duration of benefits, represented numerically (i.e., dollar or visit limits).

- Non-Quantitative Treatment Limitations (NQTLs) – Non-numerical benefit limitations, such as medical necessity reviews, prior authorizations or step-therapy requirements.

“NQTLs are primarily what the regulators are looking at now, and will look at if the final rules pass this January,” Fraker said. The proposed rules would require plans to perform comparative analysis three ways to show compliance:

- “No more restrictive” rule – The plan must use a new mathematical test to confirm that mental health and substance use disorder benefits (MH/SUD) benefits are no more restrictive than NQTL on medical/surgical benefits.

- “Design and application” rule – The plan must document that the processes, standards, strategies, and other factors used to design and apply NQTL to MH/SUD benefits are comparable to and no more stringent than those used for medical/surgical benefits.

- “Outcomes data” rule – The plan must collect and evaluate relevant data in a manner reasonably designed to assess the impact of NQTL’s access to MH/SUD and medical/surgical benefits.

While the proposed rules add detail to the NQTL comparative analysis requirement, it actually became effective under the Consolidated Appropriations Act in 2021. “Plan sponsors should already be performing and documenting the required analysis,” Fraker notes.

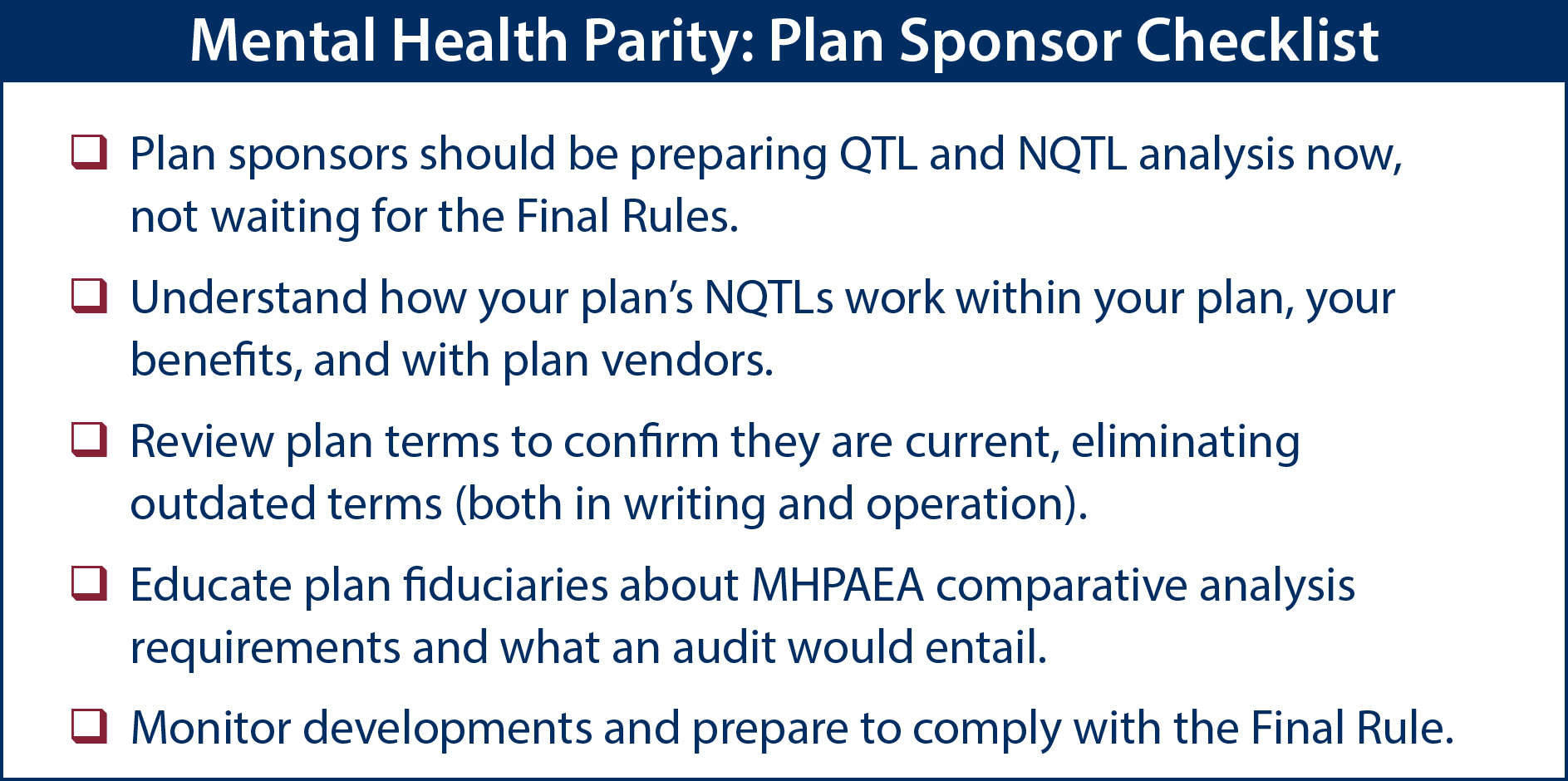

As these rules are finalized, MedBen will provide clients with additional information, as well as access to testing and comparative analysis assistance. In the meantime, we’ve compiled a checklist below to help plan sponsors prepare for the rules.